How Do Rising Interest Rates Impact Selling Your Marysville Home?

Question:

If interest rates keep rising, will it hurt my chances of selling my home in Marysville?

Answer:

Higher interest rates change how buyers behave, but they don't stop homes from selling. They affect your pricing strategy, the type of buyers you attract, and how you position your home in the market. With the right plan, you can still sell confidently in a rising-rate environment.

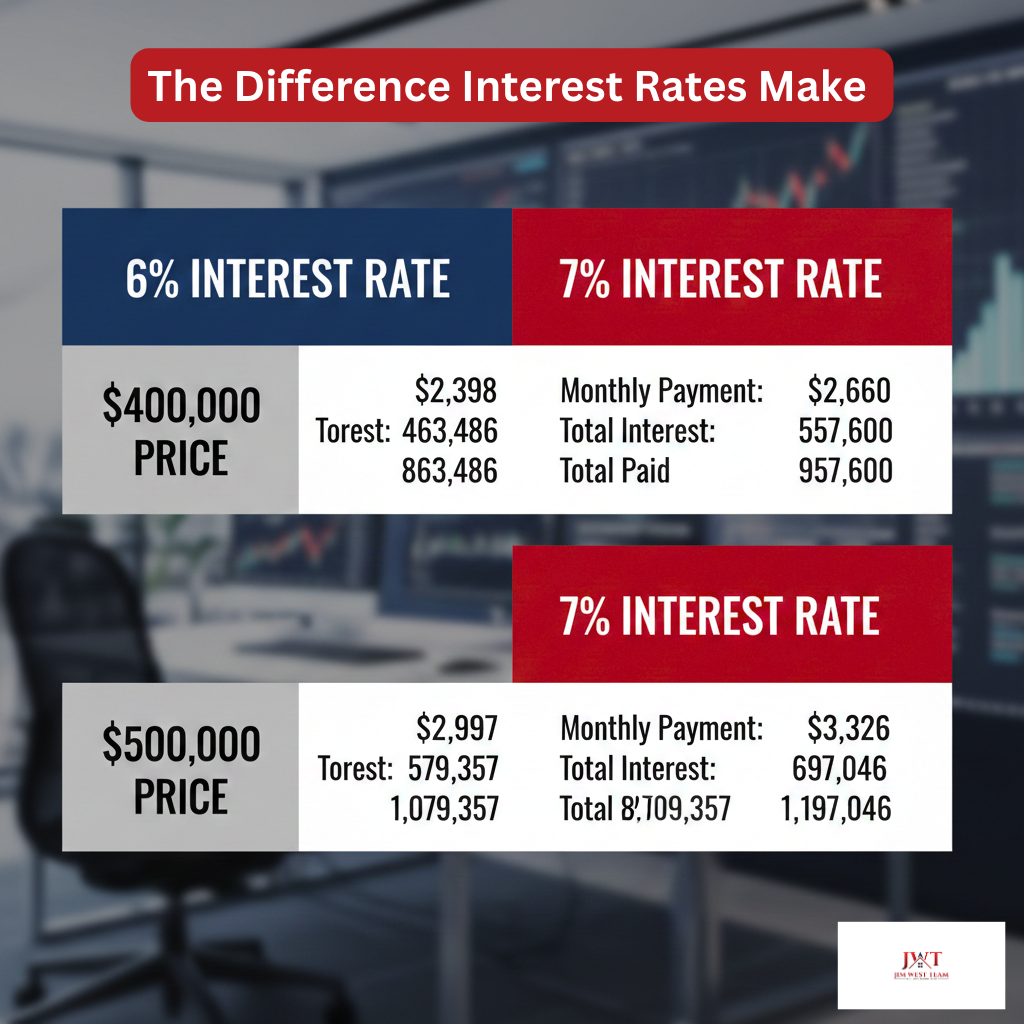

The Real Impact: A 1% rate increase means $262/month more on a $400,000 home—that's $3,144 per year or $94,320 over the life of the loan.

Understanding Today's Interest Rate Environment

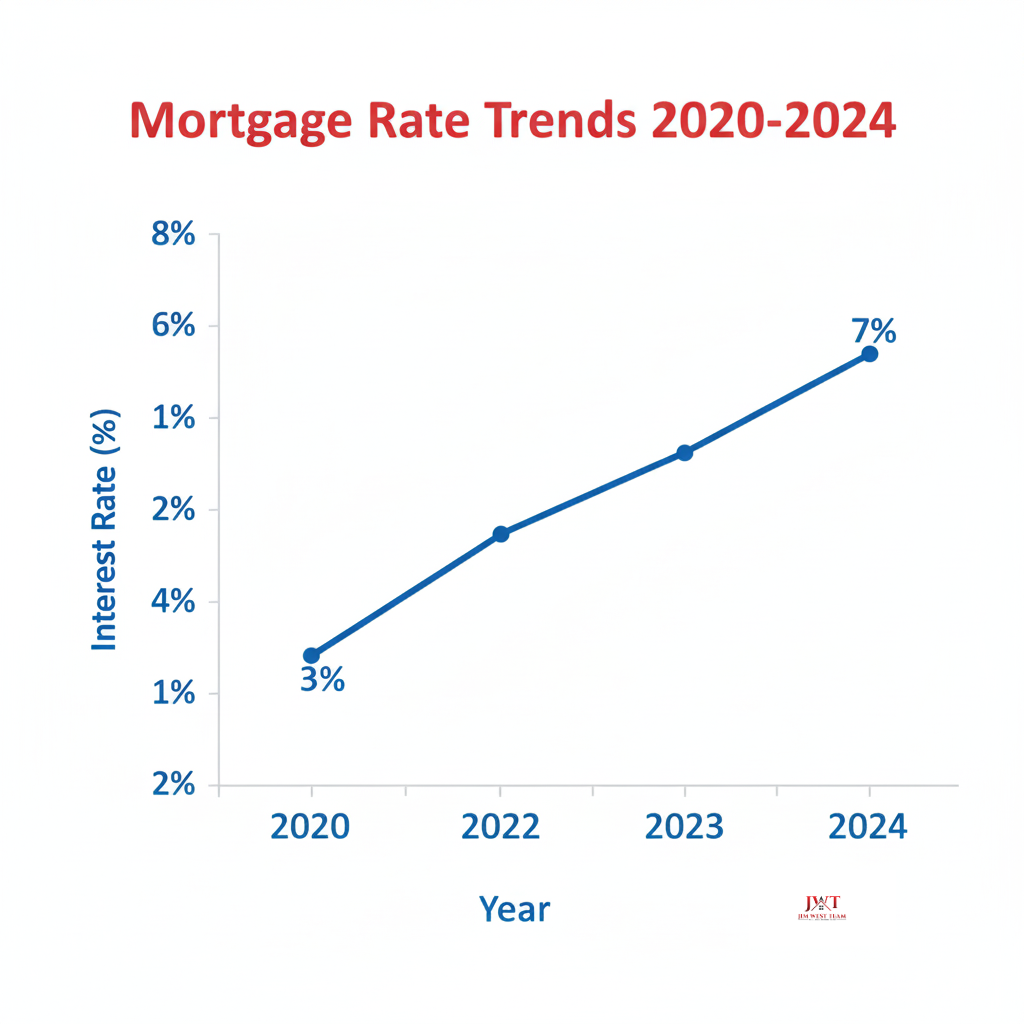

According to Freddie Mac's Primary Mortgage Market Survey, mortgage rates have fluctuated significantly over the past few years. While rates remain higher than the historic lows of 2020-2021, they're still below the long-term average of around 7-8% that was common in the 1990s and early 2000s.

Mortgage rates have more than doubled since 2020, significantly impacting buyer purchasing power and home affordability in Marysville and Union County.

For Marysville homeowners, this means understanding how these rates affect your specific market is critical. The good news? National Association of Realtors data shows that homes continue to sell in all rate environments—the key is adapting your strategy to match buyer behavior.

How Rising Rates Affect Today's Sellers in Marysville

Interest rates are one of the biggest drivers of buyer activity. When they go up, mortgage payments increase and some buyers pause their search. In Marysville, though, steady demand and limited inventory mean rising rates impact the process more than your ability to sell.

1. Buyer Demand Shifts, Not Disappears

Higher mortgage rates reduce buyer purchasing power, which leads to changes such as:

- Some buyers dropping to a lower price point.

- Others delaying their move until rates feel more comfortable.

- Motivated buyers—relocating for work, growing families, downsizing, divorce—staying active.

In Marysville specifically, demand is supported by local job growth tied to the Columbus region's expanding economy, strong schools, and continued interest in neighborhoods like Mill Valley, Adena Pointe, Green Pastures, and Hickory Run. The buyers don't disappear; they simply become more selective.

2. Pricing Strategy Becomes Even More Important

When rates rise, buyers focus harder on value. Overpricing can lead to longer days on market, weaker offers, and price reductions.

A strong pricing plan should:

- Use current comparable sales, not last year's hot market.

- Account for how rising rates affect your target buyer's budget.

- Position your home as the best value in its price range and condition.

In a rising-rate environment, correct pricing wins showings—and showings win offers. A professional comparative market analysis (CMA) from the Jim West Team provides the data you need to price competitively in Union County's current market.

3. Buyers Look for Move-In Ready Homes

Higher rates often mean buyers have less cash left over for repairs or upgrades after closing. As a result:

- Well-maintained, move-in ready homes attract stronger offers.

- Homes needing updates may still sell, but often at a discount.

- Even simple improvements—fresh paint, updated lighting, clean landscaping—can make a noticeable difference.

In a higher-rate market, buyers are more selective—these six preparation steps help your Marysville home stand out and justify your asking price.

Investing a little time and money into preparation can help your Marysville home stand out, especially when buyers are more payment-conscious.

4. You May See Fewer, But Stronger Offers

When rates are low, almost everyone jumps into the market. When rates rise, some casual shoppers step aside and the more serious buyers remain.

For sellers, that can mean:

- Fewer total showings, but higher-quality buyers.

- Offers from people who are pre-approved and ready to move.

- More focused negotiations instead of a frenzy of low-quality interest.

Well-priced homes in desirable Marysville neighborhoods still receive solid offers, even with higher rates.

5. Monthly Payment Matters More Than Just the Price

In a rising-rate market, buyers pay attention to the monthly payment as much as the purchase price. According to mortgage industry data, even a 1% increase in interest rates can add hundreds of dollars to a buyer's monthly budget. Use a mortgage calculator to see exactly how rate changes impact affordability.

That's why some sellers choose to offer:

- Rate buydowns to temporarily lower the buyer's payment.

- Closing cost credits so buyers can keep more cash on hand.

- Flexible timing so buyers can coordinate their move more easily.

These options can help your home feel more affordable without simply cutting the list price.

6. Consider Making Your Low-Rate Mortgage Assumable

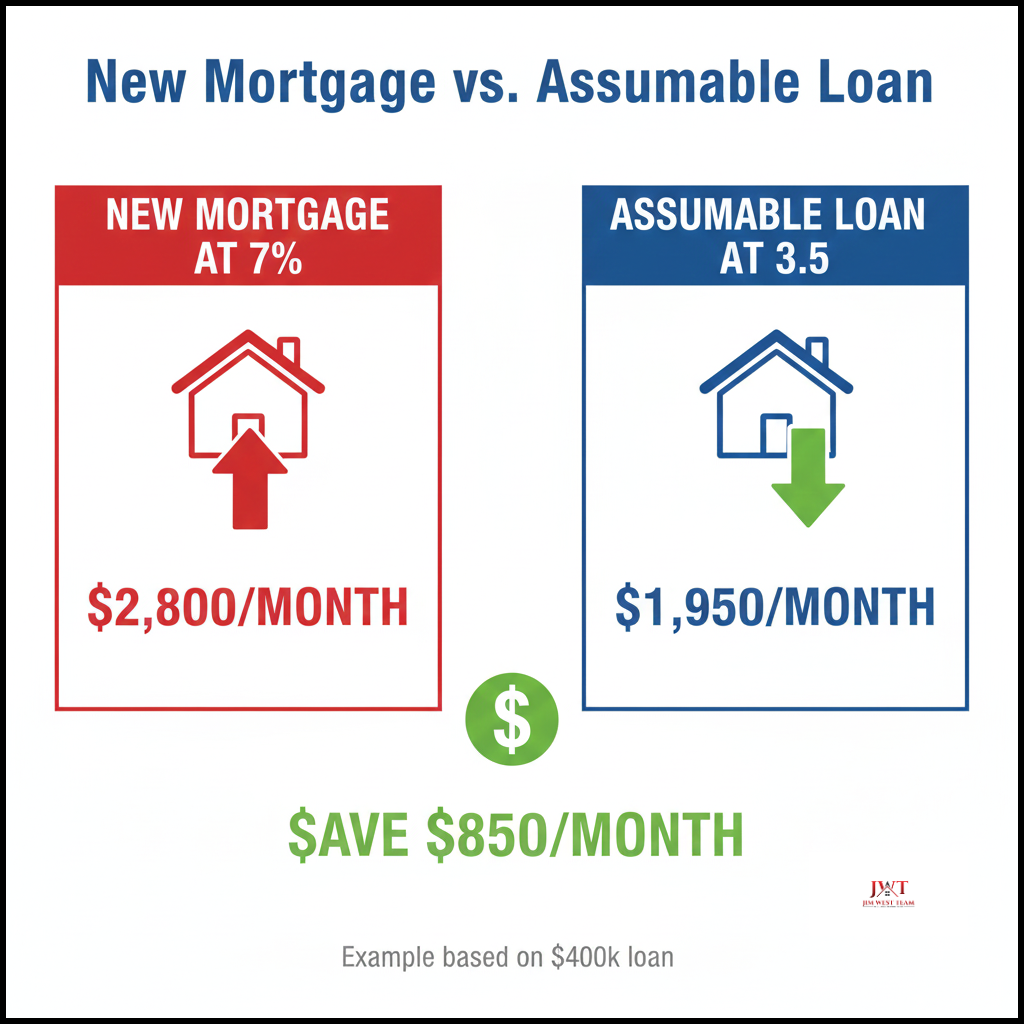

If you have a low-interest-rate mortgage from 2020-2022, you may be sitting on a powerful selling advantage: an assumable loan.

An assumable mortgage allows a qualified buyer to take over your existing mortgage—including your lower interest rate—rather than getting a new loan at today's higher rates. This can be a game-changer for buyers and make your home significantly more attractive.

Powerful Seller Advantage: If you have a low-rate FHA, VA, or USDA mortgage from 2020-2022, an assumable loan could save buyers $850+/month—making your Marysville home significantly more attractive than comparable listings.

How Assumable Loans Work for Sellers:

- FHA, VA, and USDA loans are typically assumable (conventional loans generally are not).

- The buyer must qualify with your lender and meet credit/income requirements.

- The buyer needs to cover the difference between your loan balance and the sale price (either with cash or a second mortgage).

- Processing an assumption takes longer than a traditional loan, so expect 45-60 days to close.

When to Promote an Assumable Loan:

If your current mortgage rate is 2-3% lower than today's rates, highlight the assumption option in your marketing. For example, if you have a $350,000 loan balance at 3.5% and current rates are 7%, a buyer could save over $800/month by assuming your loan instead of getting new financing.

This strategy works especially well if you're selling to first-time buyers, military families (VA loans), or anyone stretching their budget in today's rate environment.

7. Competing with New Construction Incentives

In a higher-rate market, builders often get aggressive with incentives to move inventory. You'll see offers like:

- 2-1 or 1-0 rate buydowns that temporarily lower the buyer's interest rate.

- $10,000-$30,000 in closing cost credits or upgrades.

- Paid HOA fees for the first year or two.

As a resale home seller in Marysville, you have advantages builders can't match:

While builders offer rate buydowns, resale homes in established Marysville neighborhoods like Mill Valley and Green Pastures offer immediate occupancy, mature trees, and proven value—advantages builders simply can't match.

Don't let builder incentives scare you. With the right pricing and positioning, resale homes in neighborhoods like Mill Valley and Green Pastures compete very effectively—especially with buyers who want to move now instead of waiting months for construction.

8. Market Time May Increase—But Not Always

Across Union County, days on market often tick up a bit when rates rise. However, homes that are priced correctly and presented well still move quickly.

Generally:

- Move-in ready homes at or below the area's median price sell fastest.

- Homes needing work tend to stay on the market longer unless priced accordingly.

An up-to-date market analysis from the Jim West Team will show how long homes like yours are taking to sell in Marysville right now.

9. Your Next Purchase Is Impacted Too

If you're selling and buying at the same time, higher interest rates affect both sides of your move:

- Your purchasing power for the next home.

- The timing of your sale and new purchase.

- The type of financing strategy you choose.

The upside? You're selling in a market where demand is still strong, and you may have more leverage or less competition on the buy side than during ultra-low-rate bidding wars. A coordinated plan can balance both moves.

If you're navigating a complex situation—such as selling during a divorce or coordinating multiple properties—working with a Certified Divorce Real Estate Expert (CDRE) like Jim West ensures you have a strategic partner who understands the financial and emotional complexities involved.

How to Sell Successfully When Rates Are High

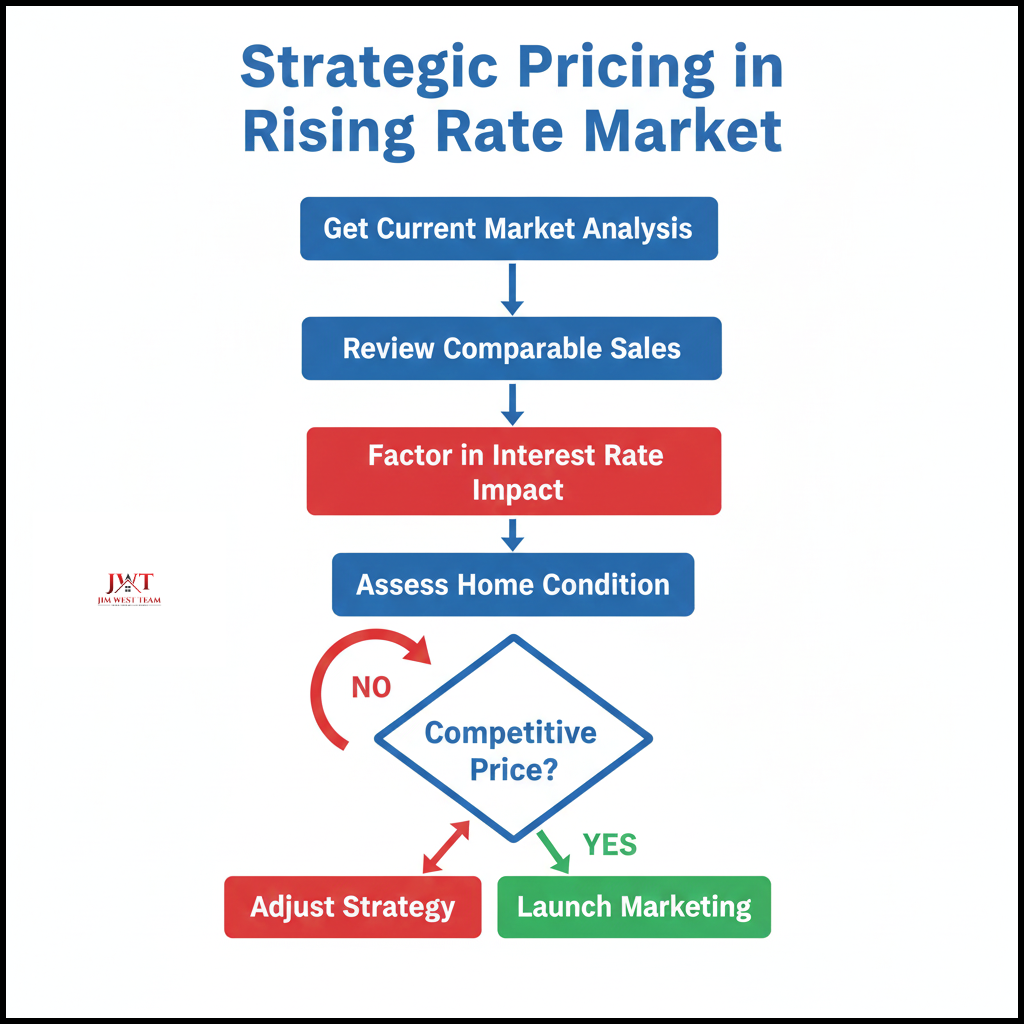

Get an Up-to-Date Market Analysis

Rates can move quickly, and so can buyer behavior. A current comparative market analysis (CMA) helps you understand pricing, competition, and expected days on market for your specific neighborhood and price range.

Follow this proven pricing process to position your Marysville home competitively when interest rates are high. The key is factoring buyer affordability into your strategy from day one—not reacting with price drops later.

Improve Your Home's Condition

In a higher-rate environment, buyers want homes that feel worth the payment. Focus on:

- Decluttering and deep cleaning.

- Minor repairs you've been putting off.

- Fresh paint in neutral colors and simple curb appeal upgrades.

Check out our comprehensive home preparation guide for specific recommendations.

Highlight Affordability in Your Marketing

Call out features that help with long-term costs, such as:

- Newer roof or windows.

- Energy-efficient systems or appliances.

- Reasonable property taxes and HOA dues (if applicable).

- An assumable low-rate mortgage (if you have an FHA, VA, or USDA loan).

Consider Buyer Incentives

Instead of a big price drop, sometimes a smaller credit or rate buydown is more powerful. Talk with your agent and a local lender about options that could make your home more attractive to buyers without giving away your equity. Common incentives include:

- $5,000-$10,000 closing cost credits

- 2-1 temporary rate buydown (approximately 2-3% of loan amount)

- Home warranty for the first year

- Flexible possession dates or rent-back agreements

Work With an Experienced Marysville Agent

When rates are rising, strategy matters. An experienced local Realtor like Jim West can help you:

- Set the right list price for the current market.

- Adjust quickly based on feedback and activity.

- Negotiate with buyers who are focused on their monthly payment.

- Position your home competitively against new construction incentives.

- Navigate complex situations like simultaneous buy/sell transactions or divorce-related sales.

Real Example: Selling Successfully in Marysville During Rising Rates

The Situation: In early 2023, a homeowner in Hickory Run needed to sell their 4-bedroom home to relocate for work. Rates had jumped from 3% to 6.5% in just 18 months, and they were worried about sitting on the market.

The Strategy:

- Priced the home 3% below recent comps to account for reduced buyer purchasing power

- Made $3,500 in cosmetic improvements (paint, landscaping, minor repairs)

- Offered a $7,500 closing cost credit to help with buyer's rate buydown

- Marketed the home's energy-efficient HVAC and low property taxes

The Outcome: The home received 4 offers in 12 days. The accepted offer was only 1.5% below the original asking price, and the seller netted more than if they'd priced aggressively high and had to reduce after 45 days on market.

Key Takeaway: Strategic pricing and thoughtful incentives beat "testing the market" every time when rates are higher.

Current Marysville Market Snapshot

Understanding the local market context helps you make informed decisions. While specific numbers change monthly, here's what Marysville sellers should know:

Current Marysville market conditions favor well-priced sellers: limited inventory meets steady buyer demand, with properly positioned homes selling within 30-45 days despite higher interest rates.

- Inventory Levels: Union County maintains lower inventory than the national average, meaning less competition for well-priced homes.

- Median Sale Price: Marysville home prices have remained stable despite rate increases, showing continued demand.

- Days on Market: Properly priced homes in popular neighborhoods like Mill Valley, Scott Farms, Green Pastures and Adena Pointe typically sell within 30-45 days.

- Buyer Demographics: Mix of local move-up buyers, Columbus area relocations, and families seeking Marysville's strong school district.

For the most current data specific to your neighborhood and price range, request a personalized market analysis from our team.

Frequently Asked Questions About Selling During Rising Interest Rates

Do higher interest rates mean I should wait to sell?

Not always. While higher rates can cool demand slightly, Marysville still has steady buyer interest and limited inventory. If selling now aligns with your life and financial goals, you can still have a successful sale with the right strategy. Waiting for rates to drop may take months or years—and you can't control when that will happen.

Will I still get strong offers on my Marysville home?

If your home is priced correctly and shows well, you can absolutely receive strong offers. You may see fewer total offers than in ultra-low-rate markets, but the buyers who remain tend to be serious and well qualified. In many cases, negotiating with 2-3 strong buyers is easier than managing 15 offers in a bidding war.

Can I buy and sell at the same time when rates are high?

Yes. Many Marysville homeowners still buy and sell at the same time. Tools like rent-backs, flexible closings, and detailed planning help you coordinate both moves. Your Realtor and lender can outline options based on your budget and timing. The Jim West Team specializes in coordinating complex transitions.

Should I lower my price if rates rise again?

Not automatically. Sometimes small improvements, better staging, or offering closing cost help can motivate buyers without a major price cut. Your price strategy should be based on local data, not headlines alone. Request a current market analysis to see how your competition is performing.

How much do rising rates really impact buyers?

Even a 1% increase in mortgage rates can noticeably change a buyer's monthly payment. For example, on a $400,000 loan, moving from 6% to 7% adds about $262 per month—or $3,144 per year. That's why buyers become more sensitive to value—and why pricing, condition, and incentives matter more when rates are higher.

Should I highlight my assumable mortgage in my listing?

Absolutely, if you have a low-rate FHA, VA, or USDA loan. In today's market, an assumable 3% mortgage can be worth tens of thousands of dollars in savings to the right buyer. Make sure your listing agent promotes this prominently in all marketing materials and the MLS.

How do I compete with builders offering big incentives?

Focus on your advantages: immediate availability, established neighborhoods, mature landscaping, and no construction delays. You can also offer your own incentives like closing cost credits or rate buydowns. Most importantly, price your home to reflect its true value compared to new construction in your area.

Final Thoughts

Rising interest rates don't have to derail your plans to sell your Marysville home. They simply require a more thoughtful approach to pricing, preparation, and negotiation. With a solid plan and the right guidance, you can still attract qualified buyers and move forward with confidence.

The key is working with a real estate professional who understands:

- How to price competitively in a higher-rate environment

- What buyers are looking for when affordability is stretched

- How to position your home against new construction incentives

- Creative financing options like assumable mortgages and rate buydowns

- The specific dynamics of Marysville and Union County neighborhoods

With over 20 years of experience in the Marysville market and a Certified Divorce Real Estate Expert (CDRE) designation, Jim West and his team have helped hundreds of homeowners successfully navigate changing market conditions.

Ready to Discuss Your Marysville Home Sale?

- 📞 Call or text (614) 507-5732 for a personalized selling strategy in today's rate environment.

- 📧 Email jimwest@jimwestteam.com to request a free Marysville market analysis.

- 🏡 Thinking about selling and buying at the same time? Ask about a step-by-step plan tailored to your move.

- 📊 Get a custom net sheet so you know what your sale could put in your pocket, even with rising rates.

- 💼 Navigating a complex situation? Learn how Jim's CDRE expertise can help with divorce-related sales, estate settlements, or multi-property transitions.

Disclaimer: This article is for general informational purposes only and is not legal, tax, or financial advice. Mortgage rates and market conditions change frequently. Always speak with a licensed lender, financial professional, or attorney about your specific situation. The Jim West Team follows the Fair Housing Act, RESPA, NAR Code of Ethics, and applicable state regulations.