Home Buyer Financing Help

This guide will aid you in understanding the different types of loans available to you and how to decide which loan is best for your given situation.

Understanding the Different Types of Mortgage Loans

Q: "There are so many loan options—how do I know which one's right for me?"

A: It depends on your financial situation, credit score, and how long you plan to stay in your home. The right loan balances your comfort with your goals—whether that's a lower monthly payment, minimal upfront costs, or long-term stability.

Common Types of Home Loans

1. Conventional Loans

The most common loan type, conventional loans aren't backed by the government. You'll typically need a credit score of 620+ and a down payment between 3–20%. If you put down less than 20%, you'll pay private mortgage insurance (PMI) until you reach 20% equity. These loans reward strong credit with competitive rates.

2. FHA Loans (Federal Housing Administration)

Perfect for first-time buyers or those with limited savings. FHA loans require just 3.5% down and allow credit scores as low as 580. They're government-insured, which helps lenders offer flexible terms—but you'll pay an upfront and monthly mortgage insurance premium (MIP).

3. VA Loans (Department of Veterans Affairs)

A great benefit for veterans, active-duty members, and some surviving spouses. VA loans have no down payment, no mortgage insurance, and favorable interest rates. They're one of the most affordable options for eligible borrowers.

4. USDA Loans (U.S. Department of Agriculture)

For buyers in qualifying rural or suburban areas, USDA loans offer 0% down and low rates. They're designed for moderate-income households and can make homeownership more accessible outside major cities.

5. Jumbo Loans

Used for higher-priced homes that exceed standard lending limits (over $766,550 in most areas for 2025). Jumbo loans require strong credit, higher down payments (10–20%), and more documentation. They're ideal for buyers purchasing luxury or large properties.

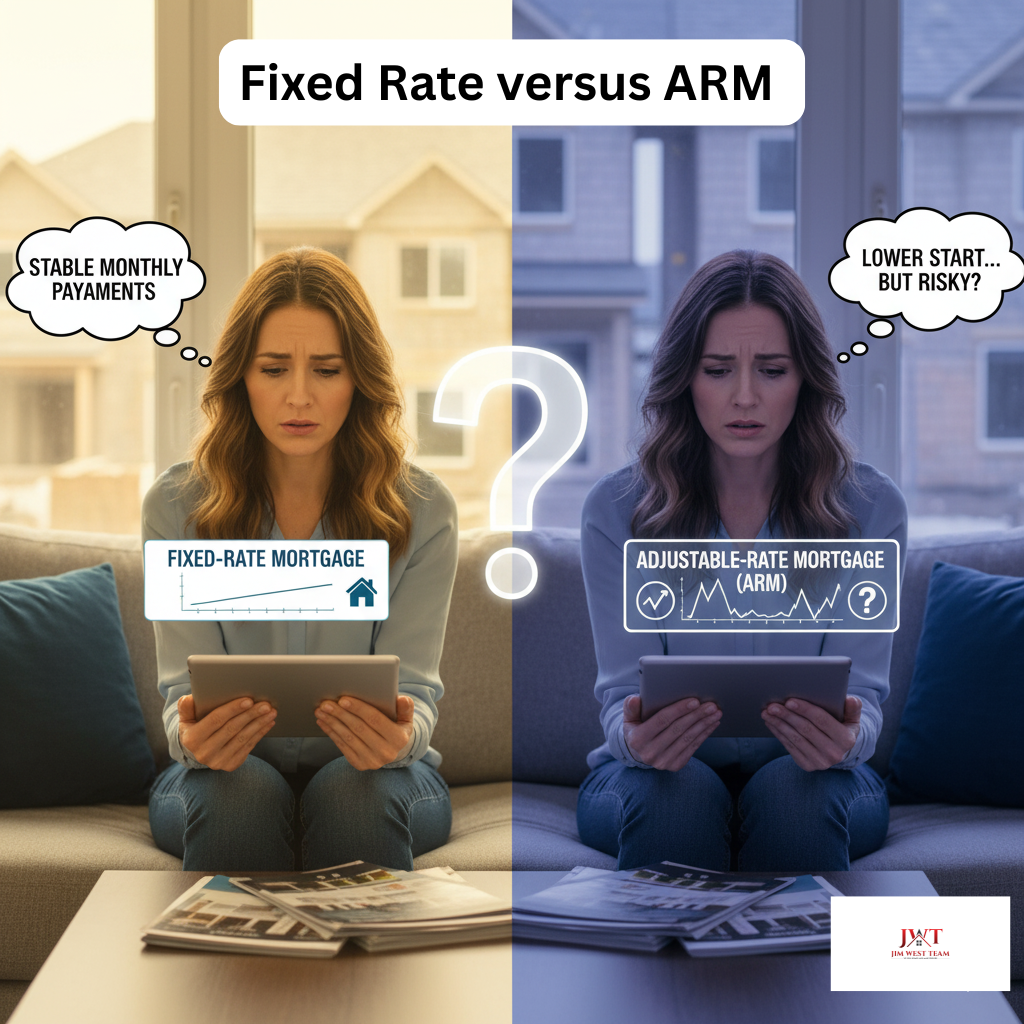

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

Fixed-Rate Mortgage

The rate stays the same for the life of the loan—typically 15, 20, or 30 years—so your monthly principal and interest never change. Best for long-term owners who value predictability and stability.

Adjustable-Rate Mortgage (ARM)

The rate is fixed for a set period (commonly 5, 7, or 10 years), then adjusts periodically based on the market. ARMs start with a lower rate, which can save money upfront, but payments can rise after the initial period. Great for buyers who plan to move or refinance before adjustments begin.

15-Year vs. 30-Year Mortgages: What's the Difference?

Choosing your loan term is just as important as choosing your loan type. Here's how they compare:

30-Year Mortgage

Lower monthly payments spread over three decades make this the most popular option. You'll pay significantly more interest over time, but the flexibility helps buyers afford more house or keep cash available for other goals.

15-Year Mortgage

Higher monthly payments, but you'll build equity faster and pay drastically less interest—often saving six figures over the life of the loan. Best for buyers with strong income who want to own their home outright sooner.

Example: On a $300,000 loan at 6.5% interest:

- 30-year: ~$1,896/month | Total interest: ~$382,000

- 15-year: ~$2,613/month | Total interest: ~$170,000

If you can comfortably afford the higher payment, a 15-year loan builds wealth faster.

Understanding Mortgage Insurance (PMI & MIP)

If you put down less than 20%, you'll likely pay mortgage insurance to protect the lender if you default.

Private Mortgage Insurance (PMI) – Conventional Loans

Costs 0.5–1% of your loan amount annually (usually $50–$150/month per $100K borrowed). The good news? You can cancel PMI once you reach 20% equity through payments or appreciation. You can also refinance to remove it.

Mortgage Insurance Premium (MIP) – FHA Loans

FHA loans charge an upfront premium (1.75% of the loan) plus an annual premium (0.55–0.85%). If you put down less than 10%, MIP lasts the entire loan term—you can only remove it by refinancing to a conventional loan.

Bottom Line: If you expect to stay in your home long-term and can eventually afford 20% equity, conventional loans offer more flexibility to drop insurance. FHA is great for getting in the door, but plan your exit strategy.

Mortgage Points & Rate Buydowns

Want to lower your interest rate? You can pay "discount points" upfront at closing.

How It Works:

One point = 1% of your loan amount and typically lowers your rate by ~0.25%. On a $300,000 loan, one point costs $3,000.

When It Makes Sense:

If you plan to stay in the home for 5+ years, buying points can save money long-term. Calculate your break-even point: divide the cost of points by your monthly savings. If you'll stay past that date, it's worth it.

When to Skip It:

If you're planning to move or refinance within a few years, keep your cash for other expenses—you won't recoup the upfront cost.

Rate Lock Tip: Once you're approved, ask your lender to lock your rate (typically for 30–60 days). This protects you from rate increases while your loan processes. Some lenders offer a "float-down" option if rates drop before closing.

How to Choose the Right Loan for You

Credit Score & Down Payment

Better credit and higher down payments unlock better rates. A score of 740+ can save you thousands over the life of your loan compared to a 640 score.

Your Debt-to-Income (DTI) Ratio

This is one of the most important numbers lenders consider. DTI = your total monthly debt payments ÷ gross monthly income.

Example: If you earn $6,000/month and have $1,500 in debts (car, student loans, credit cards, future mortgage), your DTI is 25%.

Most lenders want to see:

- 43% or lower for conventional loans

- Up to 50% for FHA loans (with strong credit)

How to Improve Your DTI:

Pay down credit cards, avoid new loans, or increase your income. Even small improvements help you qualify for better rates or larger loan amounts.

Time Horizon

If you'll stay put for many years, a fixed-rate loan is safer. Shorter-term buyers may benefit from an ARM or should consider the flexibility of lower payments.

Budget Comfort

Choose a payment you can sustain comfortably, even if life changes. Don't max out your approval amount—leave room for maintenance, emergencies, and lifestyle.

Special Eligibility

Military service? Explore VA loans. Rural property? Check USDA eligibility. These programs offer unbeatable terms if you qualify.

Closing Costs & Long-Term Expenses

Look beyond the interest rate. Review lender fees, insurance premiums, property taxes, and HOA dues. A slightly higher rate with lower fees may save money depending on how long you stay.

Pre-Qualification vs. Pre-Approval: Know the Difference

Pre-Qualification

A rough estimate of what you might afford based on self-reported income and debts. It's a soft credit check (doesn't hurt your score) and takes minutes. Useful for early planning, but sellers won't take it seriously.

Pre-Approval

A lender verifies your income, assets, and credit with documentation (pay stubs, tax returns, bank statements). You'll get a commitment letter stating exactly how much you can borrow. This involves a hard credit inquiry but shows sellers you're a serious, qualified buyer.

Why Pre-Approval Matters:

In competitive markets, sellers often won't consider offers without it. It also prevents heartbreak—you won't fall in love with a home you can't afford.

Down Payment Assistance Programs

Don't assume you need 20% saved. Many programs help buyers with down payments and closing costs:

State & Local First-Time Buyer Grants

Many states offer grants or low-interest loans (sometimes forgivable) for first-time buyers. Check your state housing finance agency's website.

Gift Funds from Family

You can use gifted money for your down payment, but lenders require a "gift letter" stating the funds don't need to be repaid. Donating family members may need to show proof of funds.

Employer Assistance Programs

Some companies offer down payment assistance or home-buying grants as an employee benefit—especially hospitals, universities, and large corporations.

Down Payment Assistance (DPA) Loans

Nonprofit and government programs offer second mortgages or grants to cover 3–5% down. Some are forgivable after you live in the home for a set period (often 5–10 years).

Ask your lender what programs you qualify for—you might be sitting on thousands in assistance you didn't know existed.

Top Questions Home Buyers Ask

1. How much should I put down?

Most loans allow as little as 3–5% down, but 20% eliminates mortgage insurance and lowers monthly costs. Put down what's comfortable while keeping an emergency fund.

2. What's the best loan for first-time buyers?

FHA and conventional 3%-down programs are common choices. The best option depends on your credit score, savings, and long-term plans.

3. How does my credit score affect my loan?

Higher scores earn lower interest rates. A 740+ score can save you tens of thousands over the life of your loan compared to a 640 score.

4. Can I buy a home with student loan debt?

Yes. Lenders focus on your debt-to-income ratio (typically under 43%). As long as your total monthly debts are manageable relative to your income, student loans won't disqualify you.

5. Should I get pre-approved before house hunting?

Absolutely. A pre-approval shows sellers you're serious, helps you understand exactly what you can afford, and speeds up the closing process once you find the right home.

6. Can I refinance later if rates drop?

Yes. Refinancing lets you secure a lower rate, switch loan types, or tap into equity. Just factor in closing costs (typically 2–5% of the loan amount) and ensure you'll save enough to make it worthwhile.

Common Mistakes to Avoid

Even savvy buyers can stumble during the mortgage process. Here's what to watch out for:

Changing Jobs Mid-Process

Lenders verify employment right before closing. Switching jobs—even for more money—can delay or derail your loan. Wait until after you've closed.

Making Large Purchases Before Closing

Financing a car, opening new credit cards, or buying furniture on credit changes your DTI and credit profile. Lenders re-check your finances before closing, and new debt can kill your approval.

Skipping Rate Comparisons

Don't accept the first rate you're offered. Shop at least three lenders—rates and fees vary significantly. Even 0.25% can save thousands over 30 years.

Maxing Out Your Budget

Just because you're approved for $400K doesn't mean you should spend it. Consider property taxes, insurance, maintenance, and lifestyle costs. Leave breathing room.

Overlooking Total Loan Costs

A lower interest rate isn't always better if it comes with high fees. Compare the Annual Percentage Rate (APR), which includes fees, not just the interest rate.

Skipping the Home Inspection

Never waive your inspection to make your offer more attractive. You need to know what you're buying. Repairs can cost tens of thousands.

Your Home-Buying Timeline

Here's what to expect from application to keys:

Pre-Approval: 1–3 Days

Gather documents (pay stubs, tax returns, bank statements) and apply. You'll receive a pre-approval letter showing your buying power.

Home Search & Offer: Varies

Could be weeks or months depending on your market and criteria. Once you find "the one," submit your offer with your pre-approval letter.

Under Contract to Closing: 30–45 Days

Your lender orders an appraisal, underwrites your loan, and verifies your finances. You'll schedule a home inspection, finalize your loan, and review closing documents.

Closing Day

Sign paperwork, wire your down payment and closing costs, and get your keys. Welcome home!

Pro Tip: Stay responsive during underwriting. The faster you provide requested documents, the smoother your closing will be.

Next Steps: Make Your Move

Ready to start your home-buying journey? Here's what to do now:

1. Check Your Credit: Pull your free credit report and address any errors. Aim for 620+ (740+ for best rates).

2. Calculate Your Budget: Use online mortgage calculators to estimate monthly payments including taxes, insurance, and HOA fees.

3. Talk to a Loan Officer: Get pre-approved and discuss which loan type fits your situation. Compare at least three lenders.

4. Save for Your Down Payment: Even 3–5% opens doors, but more is better for lower payments and better rates.

5. Connect with a Realtor: A local expert (like me!) will guide you through the market, negotiate on your behalf, and help you find the perfect home.

Have questions or ready to get pre-approved?

> If you have more questions, check out our Marysville Home Buyer Guide