The True Cost of Homeownership in Marysville, Ohio: What You'll Pay Beyond Your Mortgage in 2025

When I sit down with first-time homebuyers here in Marysville, the conversation almost always starts with one number: the monthly mortgage payment.

"Can we afford $2,000 a month?"

It's the right question to ask—but it's only part of the answer.

Over my 20+ years helping families buy homes throughout Union County and Central Ohio, I've learned that the mortgage payment is just the beginning. The true monthly cost of homeownership often runs 40-60% higher than that mortgage payment alone.

Here's the reality: The average annual cost of owning and maintaining a single-family home in the U.S., excluding the mortgage itself, is estimated at around $21,400 in 2025—roughly $1,800 per month.¹

That means a $2,500 monthly mortgage can become over $4,000 in total housing costs when you factor in property taxes, insurance, utilities, maintenance, and all the other expenses that come with homeownership.

In today's market, where nearly 45% of homeowners report post-purchase regrets—most commonly because maintenance and hidden costs were higher than expected—understanding the full financial picture before buying has never been more important.²

Let me walk you through what homeownership actually costs in our Central Ohio market, and more importantly, how to prepare for it.

Why Understanding True Ownership Costs Matters in Marysville

Qualifying for a mortgage answers one question: "Can a bank trust you with this loan?"

It doesn't answer the more important one: "Can you comfortably maintain this lifestyle?"

This distinction matters even more in our local market. Marysville and Union County have seen significant growth over the past decade—new neighborhoods like Green Pastures and Adena Pointe, major employers like Honda and Scotts Miracle-Gro bringing families to the area, and property values steadily climbing.

That growth is wonderful for our community, but it also means:

- Property tax reassessments that reflect increasing home values

- Rising insurance costs as rebuilding expenses increase

- Newer homes with HOA fees that many first-time buyers haven't budgeted for

- Larger homes than what buyers previously rented, meaning higher utility costs

I've seen too many families stretch to buy their dream home, only to feel stressed when the water heater fails or the property tax bill arrives. The goal isn't to scare you away from homeownership—it's to help you buy with confidence and realistic expectations.

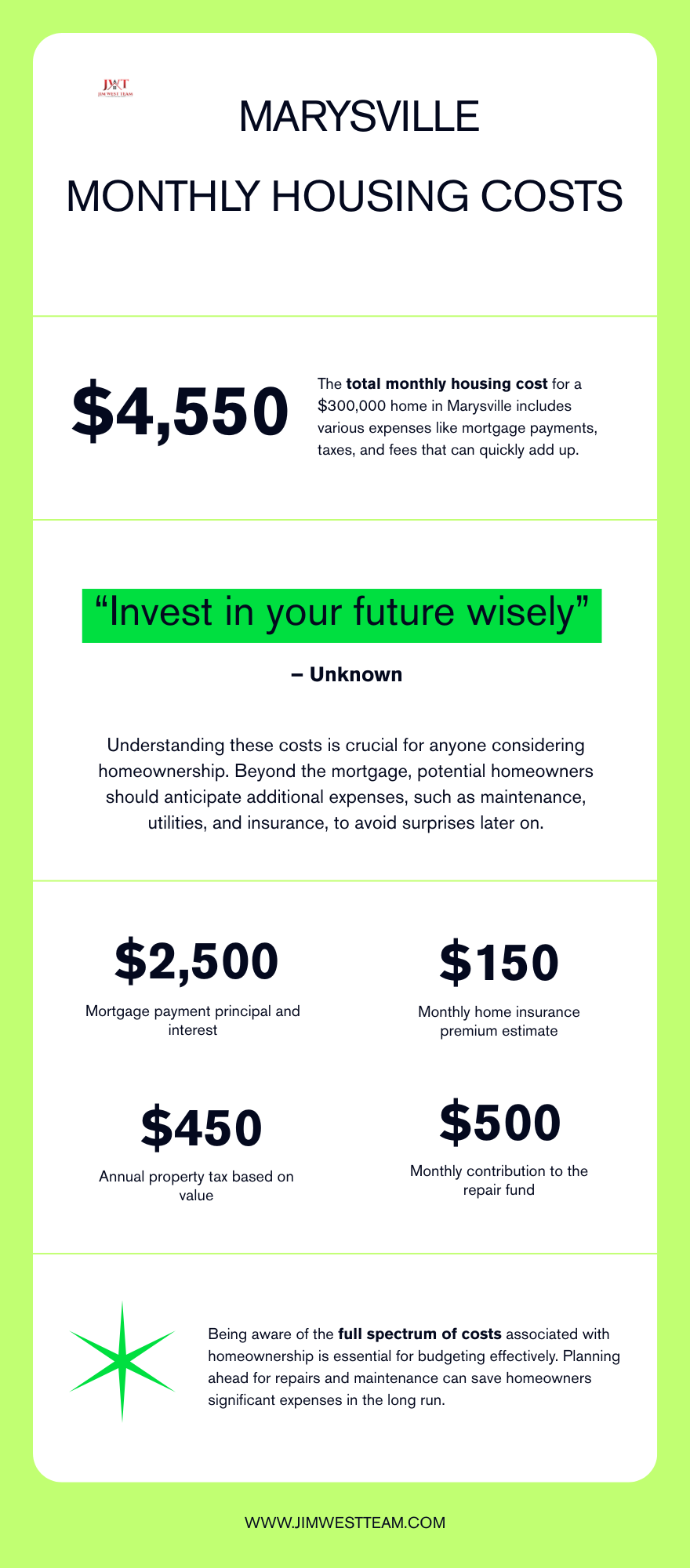

The Predictable Monthly Costs of Homeownership

These are the expenses you can plan for and budget into your monthly housing costs. While they may fluctuate year to year, they're consistent enough to build into your financial planning.

1. Property Taxes in Union County

National average: $4,271 annually (2024)³

Local context: Property tax rates in Union County vary by location and school district, but you can expect roughly 1.5-2% of your home's assessed value annually.

Here's what surprises many buyers: property taxes aren't truly fixed.

Even when tax rates stay the same, reassessments happen regularly. As neighborhood values rise—which they have significantly in Marysville over the past five years—tax bills increase accordingly.

Example: If you buy a $300,000 home in Mill Valley or Edgewood, your annual property taxes might run $4,500-$6,000. That's $375-$500 per month on top of your mortgage payment.

Property tax bills have been rising sharply nationwide, with many homeowners seeing increases of 16% or more.³ The irony? Your home's appreciation—which builds wealth—also increases your annual expenses.

Local tip: When shopping for homes, ask about recent tax reassessments and check the Union County Auditor's website for historical tax data on specific properties. This helps you budget accurately rather than being surprised a year after closing.

2. Homeowners Insurance

National trend: As of December 2025, the average premium for a new policy rose 8.5% year-over-year.⁴

In Central Ohio, we're not dealing with hurricanes or wildfires, but we face our own risks: severe thunderstorms, hail, tornadoes, flooding from heavy rains, and freeze-thaw foundation issues.

What to expect locally: For a typical $300,000 home in Marysville, annual insurance premiums generally range from $1,200-$2,000, or $100-$165 per month.

But here's the challenge: Climate disasters, higher rebuilding costs, and insurer risk recalibration continue driving these increases, and the trend shows no signs of reversing.

I've seen this happen: A homeowner's monthly payment jumps $200-300 in a single year without taking any action themselves—simply because their mortgage servicer adjusted the escrow to cover higher insurance premiums.

Local recommendation: Get multiple quotes from insurance agents who understand Union County risks. Don't just accept the policy your lender suggests—shop around and understand what's covered (and what isn't) regarding water damage, foundation issues, and wind/hail damage.

3. HOA Dues

National statistics: About 40% of homes for sale have HOA fees, with median costs around $125 per month, though single-family homes typically range from $200-$300 monthly.⁵

In Marysville: Many of our newer developments—Green Pastures, Adena Pointe, Scott Farms, The Meadows—include HOA fees that cover lawn maintenance, snow removal, common area upkeep, and sometimes amenities like pools or playgrounds.

What you need to know:

- HOA fees rarely decrease and often increase 3-5% annually

- Special assessments can add thousands in unexpected annual costs (roof replacement on clubhouse, road repairs, etc.)

- Monthly HOA dues are part of your debt-to-income ratio when qualifying for mortgages

Before buying in an HOA community: Request the HOA's financial statements, recent meeting minutes, and reserve fund status. This tells you whether the association is financially healthy or likely to hit members with special assessments soon.

Some buyers love HOAs for the maintenance-free lifestyle. Others prefer the freedom of no HOA rules. Neither is wrong—but you need to budget for it and understand what you're committing to.

4. Utilities: Bigger Homes Mean Bigger Bills

National average: Energy and utility costs averaged $4,494 annually in 2024, with internet and cable adding another $1,515.¹

The local reality: Buyers moving from apartments to single-family homes in Marysville often see these costs double due to:

- Increased square footage (heating/cooling 1,800 sq ft versus 900 sq ft)

- Natural gas heating (common in our area) plus electric

- Water and sewer (significantly more expensive for homeowners)

- Outdoor irrigation during Central Ohio's hot summers

- Multiple-story climate control in two-story homes

Budget for: $300-$500 per month for utilities in an average single-family home, with higher costs during summer (AC running constantly) and winter (heating a full house).

Energy efficiency matters: Homes built in the last 10-15 years generally have much better insulation and efficient HVAC systems than older properties. A well-insulated newer home might cost $300/month to heat and cool, while a 1980s home with original windows could run $500+ in extreme months.

5. Routine Maintenance Services

Beyond emergencies, homes require ongoing care. For many busy families working at Honda, Scotts, or commuting to Columbus, these aren't luxuries—they're practical solutions to time constraints.

Common routine expenses:

- Lawn service: $150-$300/month (April-October)

- Snow removal: $300-$600 per season

- Gutter cleaning: $150-$250 twice yearly

- Pest control: $40-$80/month

- HVAC servicing: $200-$300 annually

- Septic pumping: $300-$500 every 3-5 years (if applicable)

Collectively, these services can add $200-$400 monthly to ownership costs—even more if you have a larger lot or complex landscaping.

Local consideration: Many Marysville homes sit on 0.25 to 0.5-acre lots. That's wonderful for space and privacy, but it also means more lawn to maintain, more landscaping to care for, and more driveway to plow.

The Irregular—But Inevitable—Expenses

This is where many homeowners get caught off guard. These aren't monthly bills, but they're guaranteed to happen eventually. The question isn't "if" but "when"—and recent years have made "when" far more expensive.

Major System Replacements and Repairs

Home maintenance now averages around $8,800 annually, with first-year homeowners often facing even higher costs.¹,⁶

Here's what major repairs actually cost in 2025:

| System/Repair | Typical Cost | Expected Lifespan |

|---|---|---|

| HVAC replacement | $5,000-$10,000 | 15-20 years |

| Roof replacement | $8,000-$15,000 | 20-25 years (asphalt shingles) |

| Water heater | $1,200-$2,500 | 10-12 years |

| Foundation repairs | $4,000-$12,000 | Varies by severity |

| Sump pump | $800-$1,500 | 7-10 years |

| Garage door + opener | $1,200-$2,500 | 15-20 years |

| Appliance replacement (each) | $600-$2,000 | 10-15 years |

These aren't possibilities—they're certainties with varying timelines.

Using Your Home Inspection as a Planning Tool

When I represent buyers, I emphasize this: The inspection isn't just about negotiating repairs—it's about building a financial roadmap for ownership.

Example from my experience: Last year, I helped a family buy a beautiful home in Mill Valley. The inspection revealed:

- 15-year-old water heater

- 18-year-old HVAC system

- Roof with 5-7 years of remaining life

The systems were all functional—nothing "failed" the inspection. But this told us the buyers should budget for approximately $15,000-$20,000 in likely expenses within the first 5 years.

That's not a deal-breaker. It's a budget roadmap.

Armed with this information, the buyers:

- Negotiated a modest price reduction

- Created a dedicated home repair fund

- Started with the water heater replacement right away (cheapest fix)

- Began planning for the bigger expenses

Compare that to being blindsided three years later when the HVAC dies during a July heat wave and you're scrambling to find $8,000 immediately.

Newer Homes Aren't Maintenance-Free

I often hear: "We're buying new construction, so we won't have repair costs for years."

Newer builds offer a temporary reprieve and come with builder warranties (typically 1 year comprehensive, 10 years structural). But:

- Systems still age: That HVAC system starts its countdown to replacement from day one

- Warranties expire: After year one, you're on your own for most repairs

- Builder-grade components: New construction often uses builder-grade appliances, flooring, and fixtures that may need replacement sooner than expected

- Landscaping maturity: New yards need significant work and investment in the first few years

Eventually, every home requires major capital improvements, regardless of age.

Emergency Repairs Happen at the Worst Times

This is Murphy's Law of homeownership: Problems arise when it's least convenient and most expensive.

- HVAC failure during a heat wave (when every HVAC company is slammed)

- Burst pipe in winter (requiring emergency plumber rates)

- Storm damage to the roof (when contractors are booked solid)

- Sump pump failure during spring rains (hello, flooded basement)

Without liquid reserves, a single emergency can derail finances entirely—often forcing homeowners onto high-interest credit cards or home equity lines they hadn't planned to use.

The Hidden Truth: "Fixed Costs" Aren't Actually Fixed

Here's what surprises many first-time buyers in Marysville: the so-called "fixed costs" of homeownership aren't actually fixed.

While a locked-rate mortgage provides payment stability, the escrowed components—taxes and insurance—can climb significantly year over year.

The Escrow Adjustment Letter

Picture this scenario (which I've seen countless times):

You bought your home two years ago with a $2,200 monthly payment. The payment felt comfortable. You budgeted accordingly. Everything's fine.

Then a letter arrives from your mortgage servicer:

"Due to increased property taxes and insurance premiums, your new monthly payment will be $2,465, effective next month."

No move. No refinance. No renovation.

Yet your annual housing costs just jumped $3,180 per year ($265 × 12 months).

This happens because:

- Property reassessment increased your tax bill by $1,200 annually

- Insurance premium increased by $900 annually

- Escrow shortage from underestimating previous year's costs added $1,080

The Creep Effect on All Ownership Costs

The same gradual increase affects every aspect of homeownership:

- Utilities: Rates increase 3-5% annually

- Maintenance services: Labor and materials costs rise with inflation

- HOA fees: Annual increases written into bylaws

- Property insurance: Rising rebuild costs and weather risk

- Replacement costs: That $7,000 HVAC from 5 years ago now costs $9,500

Budgeting for homeownership means expecting costs to rise 3-5% annually. True stability requires planning for volatility.

A mortgage payment that felt comfortable at closing can feel tight three years later, even without any lifestyle changes.

Marysville-Specific Considerations for Homebuyers

Having worked in this market for over 20 years, I've learned our area has unique characteristics that affect ownership costs:

Property Types and Cost Implications

Established neighborhoods (Mill Valley, Edgewood, Central Marysville):

- Older homes with mature trees and landscaping

- Potentially aging systems (HVAC, roof, plumbing)

- Lower HOA fees or no HOA

- Higher maintenance needs but more character

Newer developments (Woods @ Mill Valley North, Adena Pointe, Scott Farms):

- Modern systems with warranties

- HOA fees for maintenance services

- Energy-efficient construction (lower utilities)

- Less established landscaping (initial investment needed)

Rural properties (outside city limits):

- Septic systems (pumping costs, potential repairs)

- Well water (pump replacements, water quality testing)

- Propane heating (more expensive than natural gas)

- Longer driveways (more snow removal costs)

- Private road maintenance costs

Climate Considerations

Central Ohio's weather creates specific ownership challenges:

- Freeze-thaw cycles: Foundation stress, pipe bursts, ice dams

- Heavy summer storms: Roof damage, tree damage, flooding

- High humidity: HVAC strain, basement moisture issues

- Temperature swings: Energy costs spike in extreme months

Commuter Considerations

Many Marysville residents commute to Columbus, Dublin, or Delaware for work. Factor in:

- Vehicle maintenance: Higher mileage means more frequent repairs

- Fuel costs: 30-45 minute commutes add up

- Time costs: Less time for DIY home maintenance

This often means hiring services you might otherwise handle yourself, adding to monthly ownership costs.

Planning Smarter: How Marysville Homeowners Can Stay Ahead

The encouraging news: buyer's remorse is largely preventable.

The issue isn't buying the wrong house—it's buying without adequate preparation. Here's how to set yourself up for success:

1. Create a Dedicated House Repair Fund

Separate from your emergency savings, this fund exists solely for home maintenance and repairs.

Treat it like a non-negotiable monthly bill: Set up automatic transfers so it happens without thinking about it.

How much to save:

The old rule of saving 1% of your home's value annually? It's outdated.

Plan for more—closer to 2-3% of your home's value annually, or whatever amount lets you sleep at night knowing an HVAC failure won't derail your budget.

Example: For a $300,000 home:

- 1% rule: $3,000/year = $250/month

- Realistic target: $6,000-$9,000/year = $500-$750/month

That might sound like a lot, but remember: you're not spending it every month. It accumulates until needed, creating a cushion for inevitable repairs.

Start small if needed: Even $200/month builds to $2,400 in a year—enough to cover most mid-sized repairs without panic.

2. Don't Drain Your Savings at Closing

I know the temptation: put every available dollar toward the down payment to reduce your mortgage, or dump everything into immediate upgrades and furnishings.

Resist this urge.

Cash reserves after closing protect against surprises and prevent forced debt when repairs arise.

Recommendation: Keep at least $5,000-$10,000 liquid after closing, separate from your regular emergency fund. This is your "house emergency" buffer.

That breathing room matters more than most buyers realize. It's the difference between handling an emergency water heater failure as an inconvenience versus a financial crisis.

3. Invest in Preventative Maintenance

The math is simple: A $200 annual HVAC service call that catches a minor issue costs far less than the $8,000 system replacement that happens when that minor issue becomes catastrophic failure.

Create a seasonal maintenance calendar:

Spring (March-May):

- HVAC checkup before cooling season

- Gutter cleaning after winter debris

- Roof inspection for winter damage

- Exterior paint touch-ups

- Lawn care begins

Summer (June-August):

- Check A/C performance monthly

- Inspect and clean outdoor drainage

- Tree trimming (before storm season)

- Deck/fence staining or sealing

Fall (September-November):

- HVAC checkup before heating season

- Gutter cleaning before winter

- Chimney inspection/cleaning

- Winterize outdoor faucets

- Check weather-stripping on doors/windows

Winter (December-February):

- Check for ice dams

- Monitor basement for moisture

- Test sump pump operation

- Change furnace filters monthly

- Check insulation in attic

Consistency prevents costly surprises and extends the life of major systems.

4. Know Your Home's Systems and Timelines

Understanding when major systems were last replaced helps predict future expenses.

Get this information before buying:

- HVAC age and service history

- Roof installation date and material type

- Water heater installation date

- Last plumbing inspections or repairs

- Foundation or structural work history

- Septic system service records (if applicable)

Create your own home timeline:

A 12-year-old water heater isn't an emergency today, but it signals a likely expense within 2-3 years. Planning beats scrambling.

5. Build Relationships with Quality Local Contractors

Don't wait until an emergency to find contractors. Build relationships now:

- HVAC company: Schedule annual service, get to know them

- Plumber: Use them for small jobs, save number for emergencies

- Electrician: Same approach

- Roofer: Get periodic inspections

- General handyman: For smaller repairs and projects

When you have established relationships:

- You get faster response times in emergencies

- You receive better pricing

- You trust the work quality

- They understand your home's specific needs

When Homeownership Still Makes Sense in Marysville

After reading about all these costs, you might wonder: Is homeownership even worth it?

Absolutely—when approached correctly.

Despite the expenses, homeownership remains one of the most powerful wealth-building tools available to American families. Here's why it makes sense in our Central Ohio market:

1. Long-Term Equity Building

Every mortgage payment builds equity with every payment. Unlike rent, ownership creates a forced savings mechanism that compounds over decades.

In most markets—including Marysville—homes appreciate over time, multiplying the wealth-building effect.

Local example: A home purchased in Mill Valley for $180,000 in 2010 is likely worth $280,000-$320,000 today. That's $100,000-$140,000 in appreciation alone, not counting the principal paid down on the mortgage.

2. Stability and Control

Homeowners control their living environment. Want to:

- Renovate the kitchen?

- Paint the walls whatever color you choose?

- Install a fence for your dogs?

- Build a deck?

- Add solar panels?

- Plant a garden?

Ownership provides autonomy that renting never will. That control has both lifestyle and financial value.

For families with children, there's stability in knowing you're not moving due to landlord decisions—your kids can grow up in one school district, one community, with lasting friendships.

3. Predictability vs. Rent Volatility

Here's a stark reality: National rents have climbed 31% over the past five years.⁷

While ownership costs rise gradually over time, rent increases can be sudden and dramatic—sometimes 15-20% in a single lease renewal.

The mortgage advantage: A fixed-rate mortgage provides payment predictability that renting cannot match.

Yes, taxes and insurance increase. But the principal and interest portion—typically 60-70% of the total payment—remains locked for 30 years.

Renters face volatility on 100% of their housing costs. Homeowners lock in the majority of their largest housing expense.

4. Tax Benefits

Homeownership offers tax advantages:

- Mortgage interest deduction (first $750,000 of mortgage)

- Property tax deduction (up to $10,000 SALT limit)

- Capital gains exclusion when selling ($250,000 single, $500,000 married)

Consult with a tax professional about your specific situation, but these benefits add meaningful value.

5. Lifestyle Benefits

Beyond finances, homeownership offers intangible benefits:

- Deeper community roots: Homeowners tend to invest more in their neighborhoods

- Stability for families: Children can grow up in one community

- Space for hobbies: Workshop in the garage, garden in the yard, home gym

- Pride of ownership: Building something that's truly yours

These benefits have real value, even if they don't appear on a balance sheet.

The key is ensuring the financial foundation supports the lifestyle, not undermines it.

A Better Way to Think About Affordability in Central Ohio

The true measure of affordability isn't what a lender will approve—it's what allows you to sleep well at night when the water heater fails or the insurance premium spikes.

The "Total Housing Cost" Calculation

Instead of asking "Can we afford a $2,500 mortgage?" ask:

"Can we afford $4,000-$4,500 total monthly housing costs?"

Here's what that includes: