Can You Sell Your Marysville Home With a Loan or HELOC?

Common Homeowner Question: "Can I still sell my Marysville home if I have a mortgage, HELOC, or equity loan on it?"

Short Answer: Yes — you can absolutely sell your home even if you still owe money on a mortgage or have a HELOC. Most Marysville homeowners sell before their loan is fully paid off. The key is understanding your payoff amount, how your equity works, and how your lender processes the final payoff at closing. With the right guidance, selling with an existing loan or HELOC is a straightforward, stress-free process.

Understanding How Mortgages and HELOCs Work When You Sell

When you list your Marysville home for sale, any outstanding loans secured by the property need to be paid off at closing. This includes your primary mortgage, second mortgage, home equity line of credit (HELOC), or home equity loan. The good news is that this happens automatically as part of the closing process — you don't need to scramble to pay off your loans before you can sell.

Here's how it typically works: Your title company or closing attorney orders a payoff statement from each lender showing exactly how much you owe on the day of closing. These payoffs are then deducted from your sale proceeds at the closing table. Whatever equity remains after paying off your loans, closing costs, and real estate commissions is yours to keep.

In the Marysville market, where home values have appreciated significantly over the past few years, most homeowners have built substantial equity even if they've only owned their home for a few years. This equity cushion makes the selling process smooth and profitable, even with outstanding loan balances.

What Happens to Your Equity at Closing?

Your home equity is the difference between what your home sells for and what you owe on it. Let's look at a realistic Marysville example:

Say you own a home in Mill Valley that you're selling for $325,000. You currently owe $210,000 on your primary mortgage and have a $25,000 HELOC balance you used to update the kitchen two years ago. Your total loan payoff is $235,000. After subtracting your loan balances and typical closing costs of around $12,000 (which includes real estate commissions, title fees, and other selling expenses), you'd walk away with approximately $78,000 in proceeds from the sale.

That equity is yours to use however you choose — as a down payment on your next home, to pay off other debts, for investment purposes, or simply to have in savings. The key is working with an experienced agent who can give you an accurate net proceeds estimate before you list, so there are no surprises at closing.

The HELOC Difference: What Marysville Sellers Need to Know

HELOCs work a bit differently than traditional mortgages, and it's important to understand these nuances when you're preparing to sell. A HELOC is a revolving line of credit secured by your home, similar to a credit card but with your house as collateral. You can borrow, repay, and borrow again up to your credit limit during the "draw period," which typically lasts 10 years.

When you sell your home, your HELOC lender needs to be paid off just like your primary mortgage lender. However, there's an important distinction: if you have an available balance on your HELOC that you haven't used, that doesn't affect your payoff amount. You only owe what you've actually drawn from the line.

One consideration for Marysville sellers: if you have a HELOC with a local credit union like Kenta Credit Union or a regional bank, they may process payoffs slightly differently than national lenders. Your real estate agent should coordinate with the title company to request payoff statements early in the process, ensuring everything is ready for a smooth closing.

Can You Sell If You Owe More Than Your Home Is Worth?

This is a concern for some homeowners, particularly those who purchased during the peak market in 2022 or refinanced to pull out equity for home improvements or debt consolidation. If you owe more on your loans than your home's current market value, you're in what's called an "underwater" or "upside down" position.

In the Marysville market as of late 2025, this situation is relatively uncommon because home values have remained stable and even increased slightly in many neighborhoods. However, if you do find yourself in this position, you have options. A short sale — where your lender agrees to accept less than the full loan balance — may be possible, though it requires lender approval and can impact your credit. Alternatively, you could bring cash to closing to cover the difference between your sale price and loan payoff.

Before making any decisions, it's essential to get a professional comparative market analysis (CMA) on your Marysville property. I can provide this at no cost and with no obligation, giving you a realistic picture of your home's current market value and your potential net proceeds.

Second Mortgages and Subordinate Liens

Some Marysville homeowners have multiple loans secured by their property. A second mortgage or home equity loan sits in "second position" behind your primary mortgage, meaning if you were to default, the first mortgage lender gets paid before the second mortgage lender.

When you sell, all liens against your property must be satisfied at closing, regardless of their position. The title company reviews the title report to identify every loan, lien, judgment, or other encumbrance that needs to be cleared. Each lender receives their payoff amount, and the liens are released so you can transfer clear title to the buyer.

This is one reason why working with an experienced local agent matters. I've handled hundreds of transactions involving multiple loans, and I know how to coordinate with title companies and lenders to ensure nothing falls through the cracks.

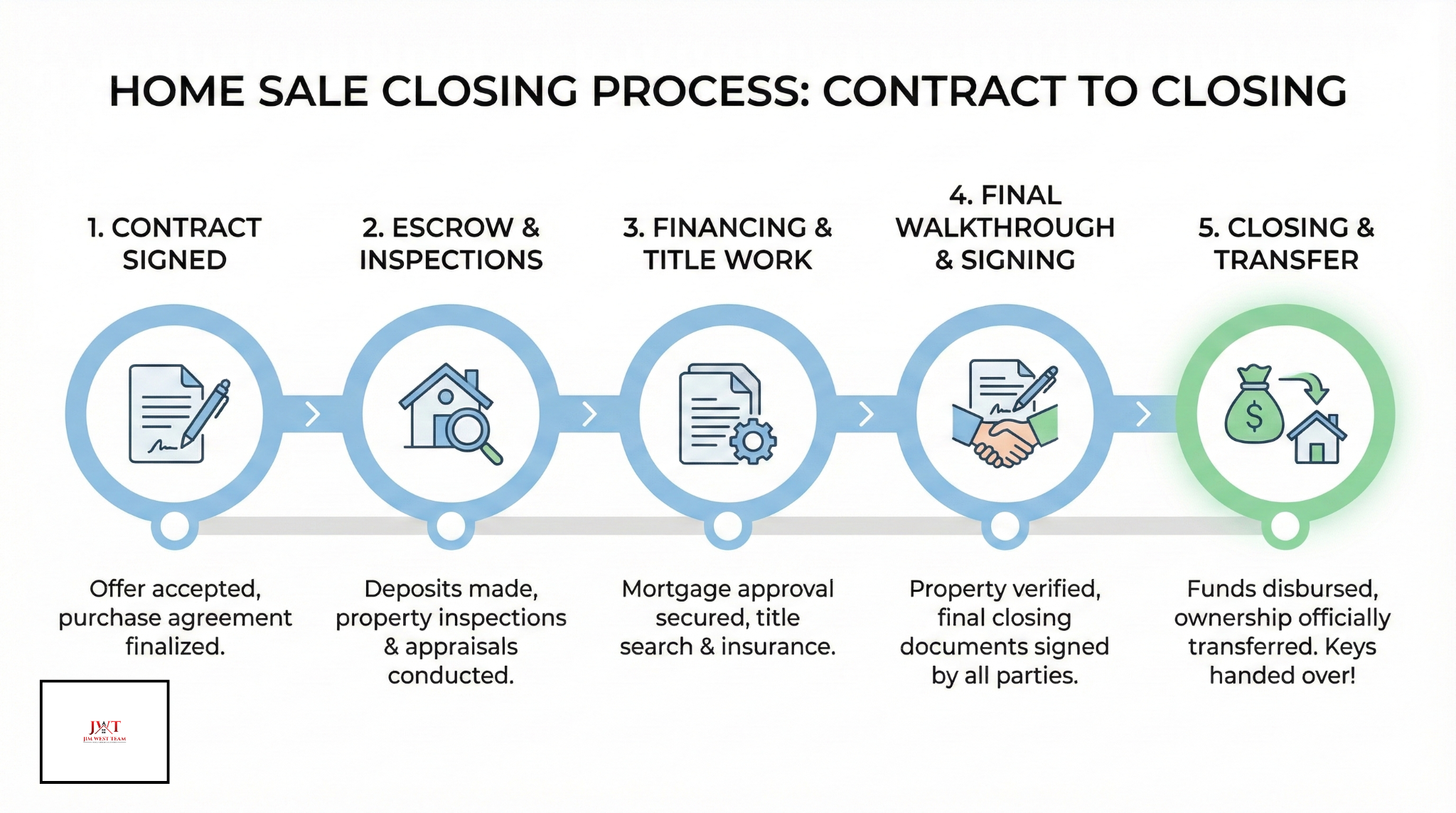

The Closing Timeline: When Your Loans Get Paid Off

Understanding the timeline helps reduce anxiety during the selling process. Here's what typically happens in a Marysville home sale:

Once you accept an offer, the title company begins working on your closing. Within the first few days, they order payoff statements from all of your lenders. These statements show the principal balance, daily interest that accrues, and the per-diem rate (how much interest adds up each day). The payoff is typically calculated to be accurate for a specific date, usually 30 days out, with instructions for how to adjust if closing happens earlier or later.

As you approach closing day, the title company prepares a settlement statement (also called a Closing Disclosure) that shows all the financial details of your sale — the purchase price, loan payoffs, prorated property taxes, homeowner association fees if applicable, real estate commissions, title insurance, and other costs. You'll review this document a few days before closing.

On closing day, you'll sign the deed and other paperwork transferring ownership to the buyer. The buyer's funds (either their cash or their lender's loan proceeds) are wired to the title company, which then distributes payments to everyone owed money: your mortgage lender, HELOC lender, your real estate team, the title company for their fees, and anyone else with a valid claim. You receive your net proceeds, typically via wire transfer to your bank account, either on closing day or within 24 hours.

What If You Used Your HELOC Recently?

This is a common question I hear from Marysville sellers. Maybe you pulled money from your HELOC last month to pay for a new roof or to consolidate some credit card debt, and now you're wondering if that affects your ability to sell.

The answer is no — you can sell regardless of when you accessed your HELOC funds. The payoff amount will simply reflect your current balance, including any recent draws. The only consideration is timing: if you accessed HELOC funds very recently (within a few days of closing), make sure to notify your agent and the title company so they can request an updated payoff statement if needed.

One thing to keep in mind: if you used HELOC funds for home improvements that increased your property's value, those upgrades can help you sell for a higher price, potentially offsetting the increased loan balance. Marysville buyers particularly value updated kitchens, finished basements, and new HVAC systems — all common uses for HELOC funds.

Refinancing vs. Selling: Making the Right Choice

Some Marysville homeowners wonder whether they should refinance their mortgage and HELOC instead of selling. This depends on your specific goals and financial situation.

Refinancing might make sense if you love your home and neighborhood but want to lower your monthly payment or consolidate debt. With interest rates currently higher than they were a couple years ago, refinancing isn't always the best financial move unless you're consolidating high-interest debt or switching from an adjustable-rate to a fixed-rate mortgage.

Selling might be the better option if you need to relocate for work, want to downsize now that kids are grown, are going through a divorce (where my CDRE designation can be particularly helpful), or simply want to take advantage of your home's equity for a fresh start elsewhere.

I can help you evaluate both options objectively, looking at your current loans, home value, market conditions, and personal goals to determine which path makes the most financial sense for your situation.

Working With Experienced Representation

Selling a home with outstanding loans doesn't have to be complicated, but it does require attention to detail and coordination between multiple parties. After more than 20 years selling homes in Marysville and Central Ohio, I've guided hundreds of sellers through this exact process.

I work closely with reputable title companies, communicate clearly with lenders to obtain timely payoff statements, and provide detailed net proceeds estimates so you know exactly what to expect at closing. My goal is to make your selling experience as smooth and stress-free as possible, whether you have one mortgage, multiple loans, or a complex equity situation.

If you're thinking about selling your Marysville home and have questions about how your mortgage, HELOC, or equity loan affects the process, I'm here to help. Reach out for a confidential, no-pressure conversation about your specific situation.

Contact Jim West

📞 Call or text: (614) 507-5732

📧 Email: jimwest@jimwestteam.com

🌐 Visit: jimwestteam.com